The global Air Quality Control System (AQCS) market is expected to grow between 2016 and 2020 at a CAGR of 7.19% with market value expected to reach around $12.8 billion by 2020 according to GlobalData’s recent report on the global AQCS market.

The main factors that will drive growth in the AQCS market toward 2020 are upcoming coal-fired plants, the adoption of emission norms and the expectation of emission norms being put in place in countries where currently there are none. Furthermore, revival of AQCS contracts is also expected to play a major role in the growth of the market.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

During the year 2015, the AQCS market in the Americas was dominated by the Flue Gas Desulfurization (FGD) segment contributing 65.7% to the market value followed by Fabric Filter (FF) with 19.5% and SCR with 14.8%. By the end of 2020, the Americas region is expected to show wide changes in the segmental sharing, wherein, it is estimated that FGD will contribute 38.6%, SCR around 28.8% and FF almost 32.6% to the market value. In the Asia-Pacific region, the FGD and the Selective Catalytic Reduction (SCR) segment both contributed a large part to the market value with 47% and 43% respectively. The remaining 10% was contributed by FF segment. Toward the end of the forecast period, the FGD market is estimated to contribute the highest towards the growth of AQCS market in the region. In the Europe, Middle-East and Africa region, 53.8% of the market value was contributed by the FGD segment, 37.9% by SCR and 8.3% by FF segment in 2015. By 2020, the SCR market is estimated to have a share of 40.4% in the total market value. The following figure shows the segmental contribution to region-wise market value during the year 2015.

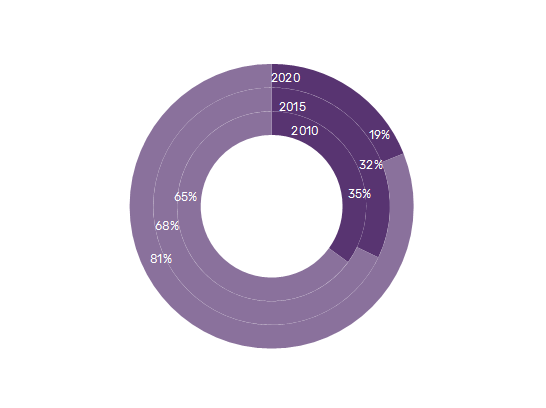

China is expected to lead the AQCS market throughout the 2010–2020 period. It has been one of the fastest growing industrial economies in recent decades. This rapid industrialization has led to a significant increase in electricity demand in the country. This has resulted in many new power plants being set up in the country. Coal-fired plants which contribute 40% of the power installed capacity in the country produce large amounts of emissions. In 2012, China was the largest contributor of carbon emission; accounting for 8.50 Gigatonnes CO2 emitted both from fossil burning and cement industries. Stringent regulations coupled with cost-effective pollution control systems have driven power plants to install emission control equipment. As a result, the country has emerged as the fastest growing market for AQCS. However, it has now started to cut down its dependence on thermal power plants and is investing more in alternative sources of energy. With its dependence on coal forecast to reduce, the AQCS systems market in China is expected to show a slowdown in growth. Nevertheless, the AQCS market in the country is significantly larger compared to those of other countries. The following figure illustrates the contribution of China on a global level in terms of market value in 2010, 2015, and 2020.