There are several strong fundamental reasons for the deployment of wind energy. Primarily, declining costs and technology advancement have enabled the technology to become one of the cheapest modes of power generation.

In 2019, the UK added 2.4GW of wind capacity, underpinned largely by offshore installations. The government has proactively pushed for offshore wind, introducing policies that have stalled onshore wind deployment, similar to solar PV. In 2019, the government proposed an installation target of 40GW for offshore wind by 2030 and recently lifted the block on onshore wind, which allows this technology to compete for long-term clean energy contracts in auctions from 2021. The government’s target of becoming carbon neutral by 2050 will prompt the development of a large number of renewable projects, which bodes well for the wind industry. With costs declining, supporting renewables is seen as a practical course of action by the government, in the transition towards emission neutrality.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The COVID-19 pandemic has resulted in economic contractions, with the pound slipping to its lowest level against the dollar. With borders being closed and strict isolation measures implemented, economic activity in the UK has slowed down significantly. As per the government’s Renewable Energy Database, nearly 15GW of wind projects, mainly offshore, are classified as ‘awaiting construction’ or ‘under construction’. “Awaiting construction” implies projects waiting to secure viable financing before initiating construction. Around 14.5GW of projects are under “awaiting construction” stage and the ongoing disruption due to COVID-19 could be a source of concern for potential investors, unless the implications can be properly evaluated and mitigated. Furthermore, future development has also been impacted, with the Round 4 offshore wind leasing round extended to provide bidders with time to consider the impacts of the pandemic in their proposals. As COVID-19 continues to weigh down on the sector, it is likely that capacity development could slow down significantly and put the sector in serious jeopardy.

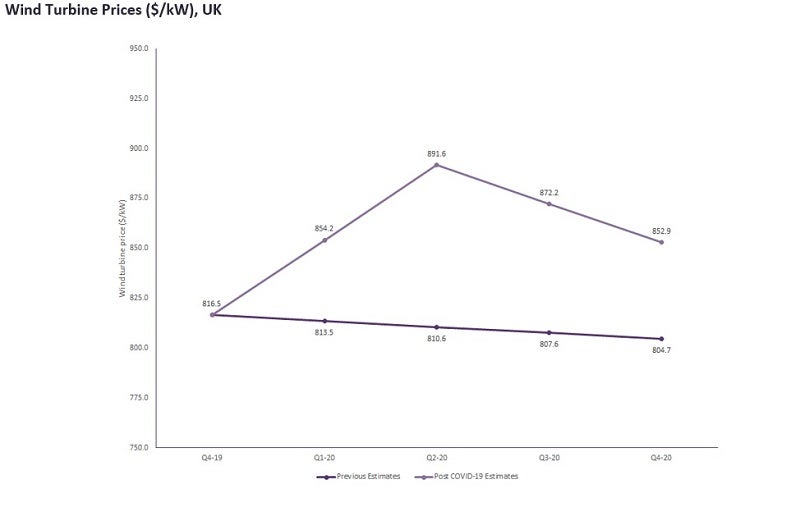

Despite being a thriving industry, the country suffers from a lack of domestic manufacturers. Several continental Europe Tier 1 wind suppliers have built manufacturing plants to serve the country’s demand. However, UK based businesses are primarily involved during development-construction, operation and maintenance, and in supplying materials as tier 2 and tier 3 suppliers, which have been integral in driving down wind costs. Nevertheless, the market stumbling blocks induced by the COVID-19 outbreak will see turbine prices increase by 4.5% between Q4 in 2019 and Q4 in 2020.

Stringent quarantine measures are likely to create a material supply bottleneck, despite manufacturing sector being exempt from the lockdown. Nevertheless, production rates are not expected to be high, driving up manufacturing costs. During quarter 1 (Q1), the price is estimated to rise to $854.2/kW and is expected to peak in Q2 to reach $891.6/kW, as suppliers across the value chain are likely to be impacted by shortage of personnel, capital crunch, and transit issues. Prominent manufacturers such as Siemens, Vestas, and Nordex have halted facilities in the major hubs of Italy and Spain, which are two of the most affected countries in the EU. However, a vast majority of Europe’s wind manufacturing plants continue to operate, with Vestas and Siemens continuing operations in the UK. The biggest impacts on the supply chain are the restrictions imposed on the movement of goods as well as workers and evolving uncertainty over policy as well as the broader UK economy. During Q3 and Q4, prices are expected to decline, as the market regains a degree of harmonization but will remain higher than the Q4 price in 2019. The prices are estimated to be $872.2/kW and $852.9/kW in Q3 and Q4, respectively.

The country is moving to improve the domestic content percentage in wind project development, as there are fears over projects being impacted by Brexit. Leaving the EU could prompt the re-evaluation of project financing models due to currency fluctuations and trade barriers. The ongoing spread of coronavirus has resulted in the emergence of a similar situation, with currency fluctuating against the dollar and borders being closed, impacting the flow of goods. In addition, commercial activities such as logistics and balance of plant support from UK businesses have declined, stalling wind deployment. The current challenges are likely to be resolved, once the lockdown measures are lifted by the government; however, the time lost in curbing COVID-19 transmission and regaining harmonization between supply and demand will most certainly result in a period of high turbine prices, which is expected to remain towards the end of 2020.