As Covid-19 continues to spread across the world and governments move to implement stringent measures to curb transmission, the solar sector in India is being constricted due to its high import dependence. China, Malaysia, and Vietnam are top countries for imports for solar power equipment, but most of the imports come from China. Shortcomings in the Chinese manufacturing sector have trickled down into the Indian market, creating uncertain times for project developers. Nearly 3GW of projects are at risk of penalties for missing deadlines, which could further add a developer’s financial strain.

With the cost of solar modules accounting for more than half the total project costs, any variation in prices could have severe implications on the overall feasibility of the project. In recent times, solar auctions in India have witnessed sharp declines in tariffs, mainly attributed to the availability of low-cost equipment from China and improvements along the supply chain. In spite of having a domestic manufacturing base, cost differentials and lack of scale to support the demand have contributed to the high imports of solar equipment, despite attracting duties.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Now, with the solar industry in China witnessing a slowdown due to the virus outbreak, developers in India are facing delays in the commissioning of projects. Solar development to support the government’s target of 100GW by 2022, which has been slow due to policy confusion, land acquisition issues, and arduous regulatory process; now faces a new threat in Covid-19. The restriction on transport in China to curb virus proliferation, has reportedly impacted the export of modules to countries including India, throwing project execution deadlines into complete disarray.

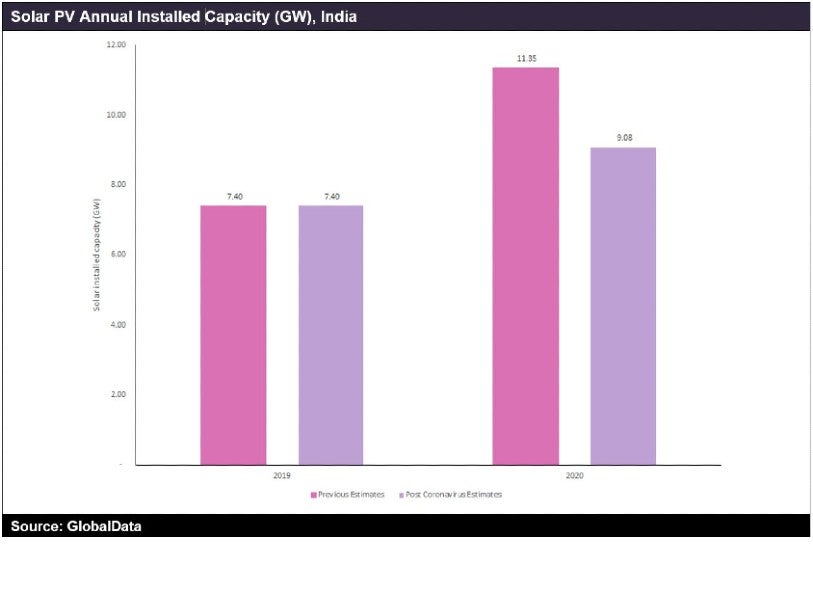

The moratorium imposed by the Chinese Government has forced several manufacturers to operate at low utilisation rates or halt operations. Moreover, modules ready to be shipped are held up in transit, due to precautionary restrictions. In order to safeguard vested interests, the government has allowed developers to invoke the force majeure clause, allowing them an additional three months for commissioning and provides both parties the option to nullify the contract, if delays extend more than 90 days. Prior to the outbreak, annual installations were estimated to reach 11.35GW in 2020, increasing from 7.4GW in 2019. However, with the ongoing issues caused by Covid-19, the lack of viable alternatives, transit delays, and the right to invoke force majeure clauses will see the estimates for solar PV annual installations decline to 9.08GW in 2020.

Uncertainty over the resolution of Covid-19 and protracted revival of the manufacturing industry in China will greatly impact the development of the solar sector in India. It is likely that project execution timelines will be pushed by a quarter, contributing to a lean installation in Q2 and new procurement strategies will need to be drawn up to support deployment in upcoming quarters. Nevertheless, this crisis provides an opportunity for the government to develop a robust domestic upstream manufacturing sector.