The size of the global wind power market increased from $21.4bn in 2006 to $94.5bn in 2017, at a CAGR of 14.4%. During 2018–2025, the wind power market size is expected to increase from $94.9 billion to $98.9bn.

A major boost in investment is due to increase in the capacity installations, led by countries such as China, the US, Germany and India, as well as emerging countries in Asia-Pacific, the Middle East and Africa (MEA) and South and Central America regions. The need for clean, reliable, and affordable power is the foremost factor for the wind power market growth. The regulatory framework and policy structure supporting wind power in various regions and countries led to significant development in the global wind power industry, and has driven the leading wind power nations in their growth trajectories.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

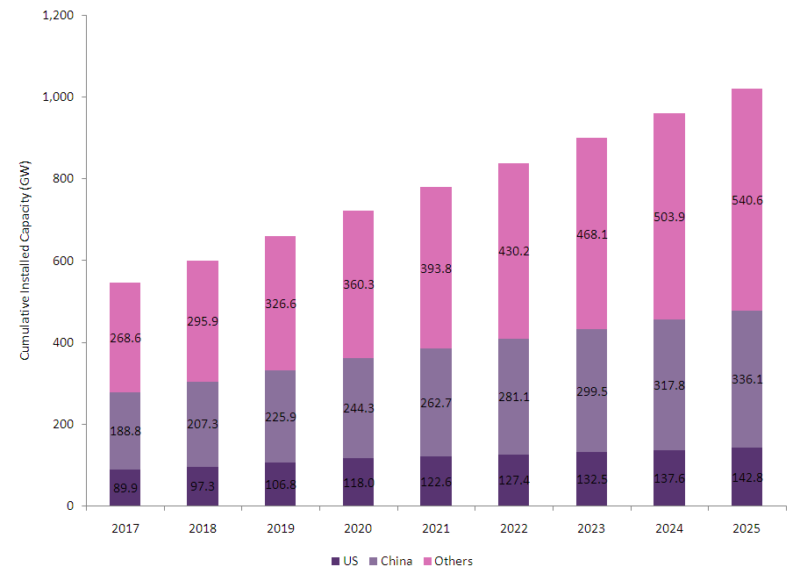

Global cumulative installed capacity for wind power increased from 74.6GW in 2006 to 547.3GW in 2017, at a CAGR of 19.9%. There was a total addition of 52.3GW in 2017 alone. In the wake of growing concerns related to energy security, increased emissions reduction targets and reduced cost of wind generation, most countries will continue to promote wind power in the coming years. Against this backdrop, the cumulative installed capacity for wind power will reach 1,019.5GW by the end of 2025.

GlobalData’s latest report, ‘Wind Power Market, Update 2018 – Global Market Size, Average Price, Turbine Market Share, and Key Country Analysis to 2025’, reveals that China is the global leader in terms of both capacity additions and cumulative wind capacity in 2017.

China and the US will continue to dominate wind installations during the forecast period of 2018-2025. China installed around 19.6 GW in 2017 and its total wind installed capacity reached 188.8 GW. China will continue to move towards a clean energy economy by adding more renewable energy sources including wind to its energy/power mix. China will continue to add wind installations in the range of 18-19 GW annually during the forecast period. Emission reduction targets, along with the investment of $360bn renewable energy by 2020 will help the wind power to grow phenomenally in the country.

The US is the second largest market after China with a share of 16.4% of the cumulative installed capacity. The country added 7.1GW of annual capacity in 2017. The wind power market of the US is driven by financial incentives, such as federal and production tax credits, which will affect the market in the short term.

Figure 1: wind power market, global, installed capacity (GW), 2017-2025

Source: GlobalData Power Database

GlobalData’s report also finds that auction-based competitive bidding has become a popular mechanism to develop wind energy in several countries. Countries including Mexico, Brazil, Argentina, Canada, Germany and India have adopted the auction mechanism for various renewable energy technologies including wind. Globally, in 2017, around 18GW of wind capacity was awarded with an average price of $49.4/MWh. In 2016, 8GW of wind capacity was awarded, which is about 10GW less than the 2017 capacity awarded. The average price in 2016 auctions was $52.6/MWh. Brazil is the pioneer in wind power auctions; the first wind auction in the country was held in 2009, and there have been several auctions in which renewable projects were provided with contracts.

Feed-in tariffs (FiTs) were the key incentive mechanism to drive the growth of wind energy up to 2016. However, due to the continuous reduction in the cost of wind power generation, auction-based competitive bidding has replaced FiTs as the most prominent mechanism to drive wind power installations in some of the key wind power markets in 2017. This trend is expected to continue in the near-term with more and more countries adopting competitive auction mechanism for wind power development.

Figure 2: wind power market, key countries, auction, 2017

Note: Bubble size represents overall capacity awarded. Source: GlobalData Power Database

The offshore wind market is expected to gain momentum during the forecast period. Offshore wind power installations accounted for 1.1% of the global wind power market in 2006, and increased to 3.4% in 2017. Offshore is being increasingly explored across the world for its high yield due to stronger and more consistent winds in comparison to onshore, and has the scope to construct massive GW-scale projects. The UK, Germany, the US and China are the major offshore wind power markets, with a number of projects currently in the planning and construction stages.

The dedicated R&D efforts of various countries are expected to drive down the cost of installing offshore wind farms. Along with this, with an increasing number of countries exploiting offshore wind potential, it is expected that the share of offshore wind in the global wind power market will reach 7.4% by 2025. In some countries such as the UK, it is expected that the offshore wind power market will surpass the dominant onshore market by 2025, driven by high offshore wind targets and contract for difference (CfD) auctions.